PART II – Fed Too Late To Prevent A Housing Market Crash?

In Part I of this research, we highlighted the Case-Shiller index of home affordability and how it relates to the US real estate market and consumer economic activity going forward. We warned that once consumers start to shift away from an optimistic view of the economy, they typically shift into a protectionist stance where they attempt to protect wealth, assets and risk of loss while attempting to weather the economic storm.

We’ve seen this happen in 2008-09 as well as after the 9/11 attacks in the US in 2001. The process is always somewhat similar. Consumers start to react to pricing levels that are unaffordable and do so by trying to skimp on extraneous purchases like travel, new cars, credit card debt or other items that are not essential. The other thing that happens is that the lower tier borrowers (the “at-risk borrowers”) typically begin to become delinquent on debts and fall behind on their mortgage payments. This is how the process starts.

Once it starts, a shift takes place in the market that can be sudden or it can be transitional. The shift is often termed as a change from a “Seller’s Market” to a “Buyer’s Market”. This terminology is used to describe who is in control of the transaction and who has the advantage within the transaction. When it is a “Seller’s Market”, buyers are typically offering to pay MORE for an item/home and the seller does not have to stress about trying to sell their property/items. When it is a “Buyer’s Market”, the buyer is able to negotiate with the seller, demanding more concessions, lower prices, better deals and often has a wide variety of sellers wanting to court the buyer away from other property/items. See how this shift in market dynamics can really change the way a marketplace works.

Be sure to opt-in to my free market research newsletter

Now, lets take a look at how the US consumer is doing, overall, and how it might reflect a change in the marketplace if certain fundamental change.

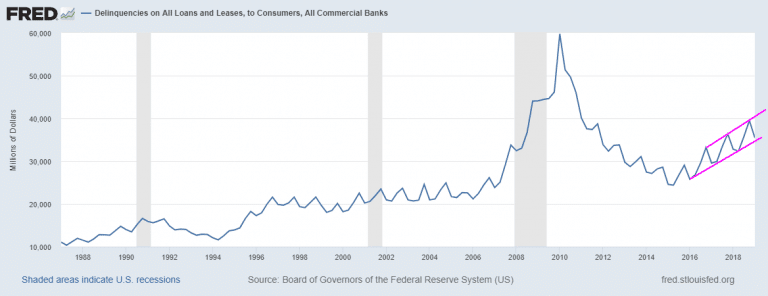

This chart of the delinquency rates for All Loans and Leases in the US shows an increase in the levels of delinquencies starting near the 2016 year. This aligns with the year that the US Fed began raising the Fed Funds Rate and is exactly 1 year after the Chinese initiated capital controls to attempt to prevent local currency (Chinese Yuan) from leaving the country and landing in other countries as foreign assets. In 2015, the delinquency rate for All Loans and Leases was near 2004~05 levels (below 30,000). Right now, the level is above the 2008 level near 36,000.

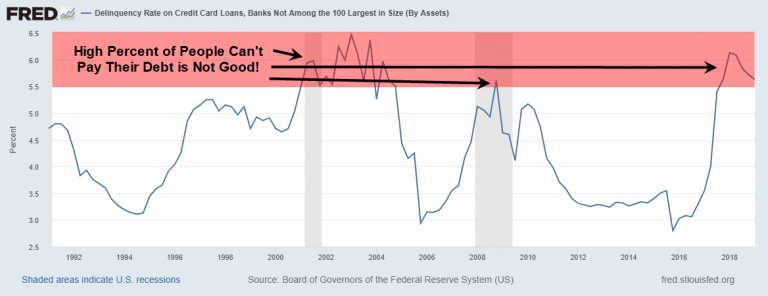

Consumer Credit Card Delinquencies are rising sharply. Since 2016, the increase in sub-prime credit card delinquencies has skyrocketed above the peak levels of 2008-09 and continues to stay above 5.5%.

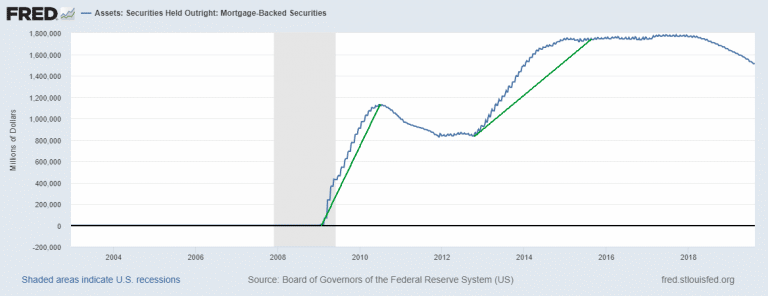

Meanwhile, those nasty Mortgage Backed Securities held outright are still massively higher than in 2008/09 based on this Fred data. We are unsure why the data is reported as ZERO in 2008, but we can safely assume that a $1.55 Trillion risk factor in these MBS levels is not something that we would consider a minor risk factor.

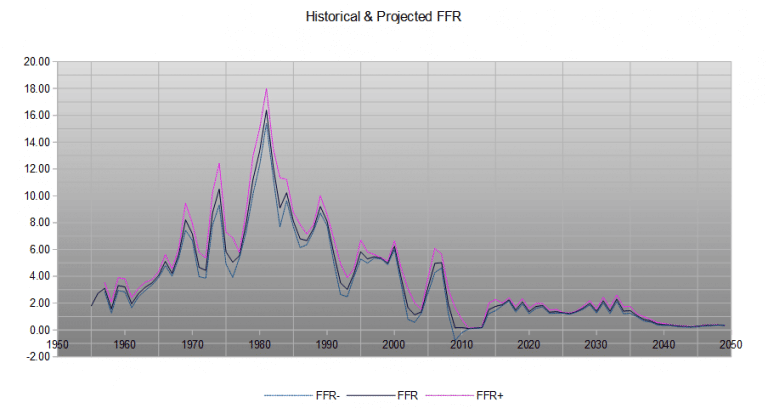

Now, in the first part of this article, we promised to show you some data from our proprietary Fed modeling utility and to show you what we use to determine if the US Fed is ahead of the curve or behind it. Here you go..

Our original research model of the US economy and the Fed Rate levels into the future are shown below. You can see that our model suggests the US Fed, as of 2013, should have been raising rates towards the 1.5% level then gradually raising them further towards 2.0% to 2.25% before 2017. This type of increase would have slowed the advance of the real estate price levels and moderated the expansion of the debt levels that are currently associated within this sector. Instead, the US Fed was late in their efforts to raise rates – starting only in late 2016.

CONCLUDING THOUGHTS:

Based on our model, current rates should be dropping toward levels near 1.25% to 1.75% as US debt, GDP and population levels continue to increase. In the 4 years after the 2020 election, rates should stay below 2% as the US Fed is somewhat trapped until GDP increases dramatically. Our modeling system suggests there are only two ways the US Fed can attempt to raise rates above 2.5% in the future; a. the US GDP increases dramatically (increasing to levels more than 1.5x total US debt annually), or b. US debt is dramatically reduced while GDP continues to grow at moderate rates.

In the last part of this 3 part article series, we’ll show you more data that will allow you to prepare for the future events that may unfold and show you how to watch for some of these trigger events yourself.

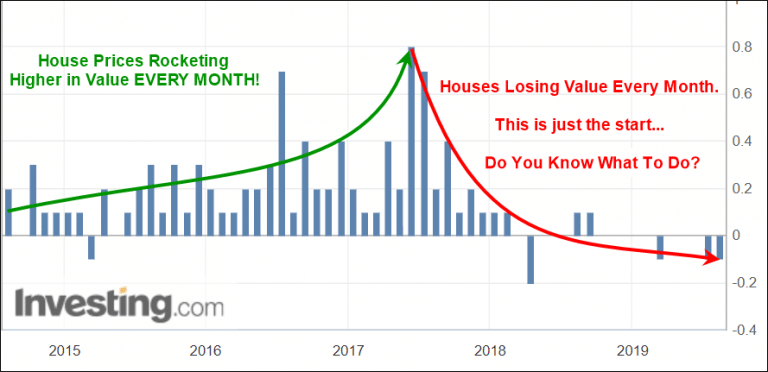

If you are like me and have friends who know nothing about real estate like cops and techie programmers building spec homes and thinking its easy money, then you know the market is or has already topped. In fact, take a look at home sales month over month in Canada.

House Values Declining Month Over Month

Real Estate has already run through the price advance cycle and the price maturity cycle. There is really only one cycle left to unfold at this point which is the “price revaluation cycle”. This is where the opportunity lies with a select real estate ETF I am keeping my eye on to profit from falling real estate prices.

I can tell you that huge moves are starting to folding not only in real estate, but metals, stocks, and currencies. Some of these supercycles are going to last years. Brad Matheny goes into great detail with his simple to understand charts and guide about this. His financial market research is one of a kind and a real eye-opener. PDF guide: 2020 Cycles – The Greatest Opportunity Of Your Lifetime

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for both short-term swing trading and long-term investment capital. The opportunities are massive/life-changing if handled properly.

I urge you to visit my ETF Wealth Building Trading Newsletter and if you like what I offer, join me with the 1 or 2-year subscription to lock in the lowest rate possible, get a FREE BAR OF GOLD and ride my coattails as I navigate these financial market and build wealth while others lose nearly everything they own during the next set of crisis’.

Chris Vermeulen

www.TheTechnicalTraders.com